China’s SME Industrial Policy in 10 Charts

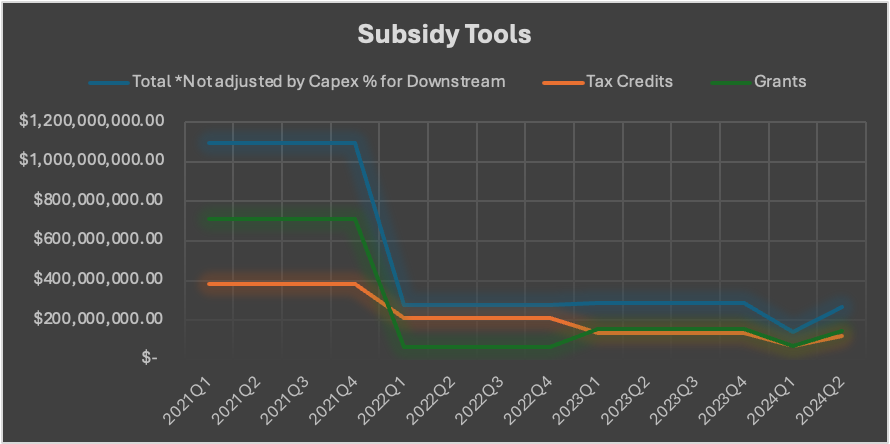

Subsidies Tools: The Fall of Tax Credits and Revival of Grants

How political are China’s chip subsidies? A few weeks ago, we saw on Chip Capitols that Beijing’s national-level political goals struggle to influence state-owned enterprises’ (SOEs) investments in the semiconductor equipment sector. This week’s article looks at China’s other major tool of semiconductor industrial policy, subsidies, to see if it is any better-oiled a political mechanism.

As before, some definitions are in order. I define subsidies to comprise tax credits and direct financial grants that the Chinese central and local governments provide to semiconductor manufacturing equipment (SME) and chip manufacturing companies, while equity investments are purchases of firms’ newly issued stock that help firms generate liquidity. Both subsidies and investments are forms of industrial policy support for SME and chipmaking companies, but China’s choice between these policy tools suggests different levels of central government coordination over which companies get helped.

Over the past few weeks, we learned on Chip Capitols that China’s equity investments into chip toolmakers are enormous but shrunk immensely during the pandemic. From a peak of $6.27 billion in central government, SOE, and private equity investments in SME firms in 2021, investment fell to a trough of $1.57 billion in 2022 during the height of China’s COVID-19 pandemic. By 2023, investment grew to $2.86 billion, which was less than half of its former height.

Furthermore, we learned that state-owned enterprises, which are absolutely political arms of the Chinese government, are not in lockstep with Beijing’s national goals. My statistics show that investments by the central government’s Big Fund have no consistent correlation with SOE investment decisions. This suggests that, despite perceptions of the PRC as a centrally planned communist monolith, Beijing has not well coordinated its industrial policies for catching up in the chip equipment sector with concurrent efforts by local governments and SOEs.

Last week, we also took our first step into subsidies, learning that grants and tax credits are a relatively small share of China’s overall industrial policy toolkit. At their height in 2021, for example, upstream SME firms received $0.87 billion from PRC government actors in subsidies (tax credits and grants), while they received $3.26 billion from government actors in equity investments.

This week, we learn that subsidies are becoming more political as the share of China’s subsidies comprised of tax credits falls and the share comprised of grants recovers.

As a reminder about this article series, many studies over the past half-decade, including here on Chip Capitols, have tried to figure out how public funds flow from the various organs of the Chinese government to the semiconductor sector. However, the use of conservative methodologies has prevented scholars from bringing forth numbers for the entire ecosystem.

I set out to compile as comprehensive data as possible on Chinese equity investments, subsidy grants, and tax credits for the country's key SME companies — regardless of whether they are public or private. This challenge required estimation based on the limited public statistics available for private companies, but it has allowed me to amass a treasure trove of charts about the Chinese SME sector.

The world deserves a first (if fuzzy) glance at the totality of China’s industrial policy for chipmaking equipment. Every week, I am releasing a new chart about Chinese government support for SME firms through (1) equity investments, (2) subsidy grants, and (3) tax credits. Today, we dive deeper into subsidies.

The Fall of Tax Credits and Revival of Grants

Tax credits and grants are fundamentally different subsidy tools. Governments can exercise maximum discretion with their grant allocations because they are awarded on case-by-case bases. In addition to the overall grant subsidy numbers in the financial disclosures from which I draw my data, many companies list out the individual sources of their grant awards. For example, of Naura’s 121.7 million RMB subsidy total in 2022, it received 30.2 million from the Beijing Municipal Party Committee Office Project (北京市委办局项目). Being relatively small, governments can withhold these grants without fearing the utter destruction of the recipient.

In contrast, tax credits are given out mechanically to companies that fit the credits’ qualifications. The central government’s largest tax credit is a 15% income tax deduction for companies designated under the Management Measures for the Recognition of High Tech Enterprises program (高新技术企业认定管理办法). Certainly, it is a political decision by the PRC Ministry of Finance whether to qualify companies for a tax credit (see here for an article I wrote in The Diplomat describing China’s tax credits). But tax credit qualification is a stickier and more financially consequential decision than individual grant awards, so government actors are likely more hesistant to use the blunt cudgel of tax credits in reaction to moderately changed political priorities. Subsidies are the scalpel best suited for reacting to modest political shifts.

Looking only at the three years covered by my analysis, some interesting trends emerge. Even though the PRC released ever larger R&D tax credits over the past few years (see, again, my 2023 article in The Diplomat), the amount of financial support China has provided the chip sector in the form of tax credits has fallen since 2021. A reason for this decline could be that tax credits are based on the scale at which companies operate. As firms’ profits decline, the size of their tax obligations also declines, so tax credits should become less valuable.

However, a look at the graph above showing the operating profits of the the companies I studied does not show a decline in 2022 to match the tax credit decline in the same year. This suggests that 2022 witnessed reductions of tax credits other than the income tax credit (which stayed stable) or the R&D tax credit (which increased). (My tax credit numbers look at the actual differences in the statutory tax obligation that a company owes and the amount that it actually pays to calculate tax credits, so it captures the effect of all credits at play. Perhaps some of these distortions are due to deferred tax payments, which the current version of this research does not account for.)

The other trend that becomes apparent in looking at the chart at the start of this article is the oscillation of grant numbers. 2022 saw a sharp fall in the value of subsidies apportioned via grants, and this makes sense in the context of COVID, where local governments faced intense financial strain. Since grants can be given or withheld relatively flexibly, it makes sense that there would be a sharp decline as soon as local governments reprioritized their resources to pandemic-prevention activities.

Later, in 2023, grants recovered while tax credits continued to fall. Knowing that the PRC chip industry’s operating profits also fell in 2023, the rise of grants that year suggests that government actors are not simply doling out support to profitable companies in their jurisdictions but rather to companies that are a political priority. This does not mean that local governments’ choice of which chip companies to invest in overlaps with central government priorities (this Chip Capitols article suggests otherwise), but the political prioritization of the chip industry as a whole does seem to withstand the sector’s economic struggles.

As each of these articles seeks to answer questions, it has the effect of raising more. Next week, we will examine how subsidy trends interact with SME firms’ and chipmakers R&D spending decisions. Stay tuned!

Methodology

Before repeating last week’s explainer on how I collected subsidy numbers, I’ll note that the total subsidy number in this article is larger than the total SME subsidy number in last week’s article. Last week, the numbers I shared were purely subsidies for chipmaking equipment. So, I discounted downstream chipmakers’ subsidies by the amount of their total expenditures spent on capex to estimate their “subsidized demand” for equipment. Since this week’s article is only interested in the breakdown of subsidies by tax credits and grants, I use the entirety of subsidies that upstream and downstream firms received.

Getting subsidy data for SME companies posed similar challenges as equity investments in that many of these firms are small and not publicly listed. To that end, I relied on liberal estimation methods.

For upstream public companies, I sourced all my data from publicly available financial reports. For upstream private companies, I tried to find at least one publicly reported statistic in Chinese media, like revenue or operating profit for each company in each year. Then, I estimated all of each company’s other stats by assuming they were proportional with the average ratios from all public companies of the same year. (For example, Shanghai Microelectronics Equipment 上海微电子was not public in 2022, but I found a report of its operating profit, which was 1.2 billion yuan. Therefore, I estimated its "statutory tax obligation" as 1.2 billion/[the average operating profits of public companies in 2022]*[the average statutory tax obligations of public companies in 2022].) This method is not accurate at the individual company level (some estimates even resulted in negative tax credits); however, it results in a reliable estimate in aggregate. More importantly, it provides macro-level insights about China’s SME subsidies that, though imperfect, can help Western government policymakers get a grasp on how much China is spending to catch up in SMEs.

Additionally, it was not enough to look only at SME companies’ financials to get a grasp of China’s countrywide support for these firms because China also subsidizes demand for semiconductor tools when it gives subsidies to the purchasers of these tools, i.e. downstream chipmakers. To that end, I examined downstream companies to estimate the “subsidized demand” for SMEs—i.e., the portion of subsidies received by downstream chipmakers that is used to purchase SMEs. I estimated the subsidized demand for each downstream company as [sum of subsidies]x[capex]/[total expenditures]. I got the underlying numbers for this section similarly as for upstream SME companies, but since most downstream chipmakers are public, I only needed to use media statistics–based estimations for two firms.

Upstream SME companies surveyed:

Advanced Micro-Fabrication Equipment Inc. China(中微公司)

Naura(北方华创)

Yitang Semiconductor(屹唐半导体)

Piotech Inc.(沈阳拓荆)

Skyverse Technology Co., Ltd.(中科飞测)

Shanghai Precision Measurement Semiconductor Technology, Inc.(上海精测半导体技术有限公司)

Shanghai Microelectronics Equipment(上海微电子)

Cetc Electronics Equipment Group Co., Ltd.(中电科电子装备集团有限公司)

Beijing Semicore Electronics Equipment Co., Ltd.(北京烁科中科信电子装备)

Shanghai Kingstone Semiconductor Corp(上海凯世通半导体股份有限公司)

RSIC Scientific Instrument (Shanghai) Co., Ltd.(睿励科学仪器(上海)有限公司)

Downstream chipmakers surveyed:

SMIC(中芯国际)

Guoxin Micro (紫光国芯)

AllwinnerTechnology (全志科技)

Changsha Jingjia Microelectronics (景嘉微)

Nations Technologies (国民技术)

Orbit (欧比特) (航宇微)

Shenzhen Goodix Technology (汇顶科技)

Datang Telecom Technology (大唐电信)

Ingenic Semiconductor (北京君正)

Hangzhou Silan Microelectronics (士兰微)

Sino Wealth Electronic (中颖电子)

Qingdao Eastsoft Communication Technology (东软载波)

GigaDevice Semiconductor (兆易创新)

Beijing Philisense Technology (飞利信)

Ninestar (纳思达)

Shenzhen Kaifa Technology (深科技)

Hua Hong Semiconductor (华虹半导体)